The latest U.S. tariff probes are not just about finished goods. They reach into shipping, semiconductors, pharmaceuticals, copper, and wood products — and that changes who carries the risk.

The U.S. is back in investigation mode, but this round matters for a different reason. The pressure is not falling only on finished goods or on one clean list of consumer imports. It is moving into shipping, semiconductors, pharmaceuticals, copper, and wood products — the inputs and trade infrastructure that many sourcing programs quietly rely on every day.[1][2][3][4][5][6]

From a sourcing perspective, that is where the real commercial risk sits. Buyers can sometimes work around a tariff when it is narrow, product-specific, and easy to model. It gets harder when the pressure hits freight lanes, derivative products, supplier documentation, and strategic inputs at the same time. At that point, the issue is not simply duty cost. It becomes a question of margin durability, supplier readiness, and whether your team actually knows where the product is exposed.[1][2][3][4][5][6]

That is why these new probes deserve more attention than the usual trade-policy headline. On paper, they look like investigations. In practice, they can reshape landed cost before a final tariff rate is even published.

What happened

The current U.S. trade posture is being shaped through a mix of Section 301 and Section 232 actions.

The maritime piece is already the clearest example. USTR determined that China’s targeting of the maritime, logistics, and shipbuilding sectors was actionable under Section 301, then followed with an announced response structure that includes phased fees tied to Chinese-linked vessel exposure and proposed action tied to port equipment.[1][7][8] That does not just affect shipowners. It creates a freight variable that importers may not control but still have to pay for.

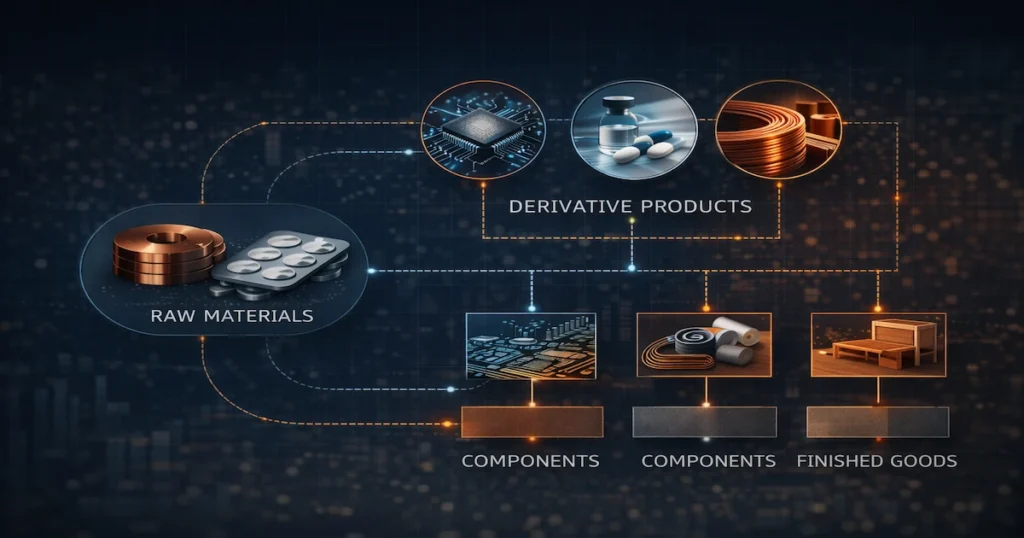

At the same time, Commerce opened Section 232 investigations into semiconductors, pharmaceuticals and pharmaceutical ingredients, copper, and timber and lumber.[2][3][4][5][6] These are not minor sectors sitting at the edge of global trade. They sit near the center of industrial sourcing, healthcare continuity, electronics manufacturing, and building-material supply chains.

What buyers often miss is that these investigations do not stop neatly at the raw material. They often reach derivative products and downstream goods. That is where exposure becomes harder to track and more expensive to fix.[2][3][4][5][6]

What this is — and what it is not

This is not just a replay of the 2018 tariff cycle.

The old trade-war framework was easier to understand because the pain was easier to locate. A category received tariffs. Buyers modeled the increase. Some shifted country of origin. Some accepted the hit. This time, the policy pressure is spreading across systems rather than only across products.

That distinction matters. If the pressure touches semiconductors, pharmaceutical inputs, copper content, lumber derivatives, and maritime capacity, the disruption moves through sourcing programs unevenly. One importer may face higher freight. Another may face supplier repricing. Another may run into origin and derivative-product questions that its current documentation cannot answer quickly enough.[1][2][3][4][5][6]

Where this breaks down in practice is visibility. A lot of importers know the final assembly country. Far fewer know the true origin profile of key inputs, the share of cost tied to strategic materials, or how exposed their lanes are to Chinese-built vessels and China-linked operators. When trade policy starts moving upstream, weak BOM discipline becomes a commercial problem very quickly.

New US Tariff Probes and who is most exposed

The most exposed companies are not always the ones importing a named product directly. Often they are the businesses sitting one layer behind the headline.

Retailers and importers of bulky, low-margin goods are exposed because freight matters more to them than it does to high-value categories. If maritime fees or carrier cost adjustments begin to move, they will feel the hit quickly. They may not see it on a tariff line first. They may see it in replenishment economics, quote validity, or lane-specific cost instability.[1][7][8]

Electronics importers are exposed for a different reason. A lot of them buy finished products assembled outside China and assume that reduces policy risk. Sometimes it does. But semiconductor-related investigations can pull attention back into the component stack. If the product depends on sensitive chip inputs, packaging ecosystems, or derivative electronic content, the exposure is still there even when the carton ships from somewhere else.[2][5]

Healthcare and pharmaceutical supply chains face a slower but more stubborn form of risk. The problem is not only cost. It is switching time. A new duty can be modeled. A new qualified source of APIs, starting materials, or finished-dose production takes much longer. That delay is often underestimated by teams used to consumer-goods sourcing.[3]

Copper-intensive manufacturers also deserve attention, especially in electrical systems, industrial assemblies, infrastructure products, and power-related components. Even before any final tariff action, an investigation can change pricing behavior. Suppliers may reprice early, hedge more aggressively, or shorten quote windows because they do not want to absorb policy risk themselves.[4][9]

Then there is wood. Furniture, cabinets, millwork, and building-product importers are used to trade friction already, but that does not mean they are protected from another layer. In fact, those categories can be some of the most exposed because they often sit at the intersection of tariff risk, AD/CVD risk, country-shift complexity, and weak documentation discipline at the supplier level.[5][6]

The operational reality buyers should not ignore

This is where the story becomes less theoretical.

Most buyers do not fail because they missed a headline. They fail because the supplier file was incomplete, the origin claim was too simplistic, the freight assumption stayed frozen too long, or the organization realized too late that a “finished good” was really a derivative product carrying upstream exposure.

In practice, the documentation burden is often underestimated. Once a category becomes strategic, the normal procurement conversation changes. Suddenly, BOM accuracy matters more. Supplier affidavits matter more. Classification reviews matter more. Contract language matters more. A supplier that looked commercially efficient six months ago can become operationally fragile if it cannot defend origin, content, or process discipline under pressure.

And this does not hit every importer evenly. A well-run sourcing team with dual-source options, strong broker coordination, and current origin files may absorb the disruption with some pain but without major damage. A buyer running on thin institutional memory, loose specifications, and supplier assurances that are not fully documented is in a different position altogether.

That is the quiet divide opening up now. The winners are not necessarily the importers with the lowest current FOB price. They are the ones that can prove what they are buying, where the risk sits, and how quickly they can shift.

Buyer impact: where margin pressure will show up first

For many companies, the first pressure point will not be the tariff itself. It will be one of the following:

- Higher freight costs tied to vessel exposure or carrier repricing.

- Supplier quote revisions as factories and traders try to pass through uncertainty before formal action lands.

- Longer internal review cycles as compliance, finance, and procurement all need to recheck exposure assumptions.

- More cautious buying behavior around SKUs with unclear derivative content or weak origin records.

- Delays in switching because alternate suppliers can quote, but cannot document.

From a Liberty Trade Chronicles perspective, that last point matters more than many buyers admit. On paper, alternative sourcing always looks available. On the ground, the alternate factory often has MOQ issues, process inconsistency, weaker BOM control, or lead times that do not work once the volume moves.

A practical decision framework

Start by separating exposure into three buckets: direct tariff exposure, freight exposure, and qualification exposure.

Direct tariff exposure is the easiest to model. If your product or a key input falls into the final scope, you can at least build a cost scenario around it.

Freight exposure is less neat. That risk moves through carriers, lanes, vessel mix, and contract structures. It can appear unevenly and create budget surprises even when the underlying product classification has not changed.[1][7][8]

Qualification exposure is usually the most dangerous because it slows response time. This is the risk that your current source becomes more expensive or more fragile, but your alternate source is not ready to carry the volume with acceptable documentation and consistency.

If a buyer understands those three buckets clearly, the response becomes more manageable. If not, every new probe starts to feel like a generalized threat, which usually leads to bad decision-making.

What buyers should do now

- Map exposure by HTS code, input content, supplier country, and freight lane.

- Identify SKUs with semiconductor, pharmaceutical, copper, or wood-product dependency.

- Ask logistics partners for visibility into Chinese-built vessel and operator exposure on major U.S. lanes.

- Review current supplier files for BOM discipline, affidavits, and origin support.

- Rework landed-cost models to include freight shifts, pass-through language, and alternate-source assumptions.

- Pressure-test alternate suppliers for documentation quality, not just price and capacity.

- Review contracts for tariff sharing, fee pass-throughs, and quote validity protections.

- Build moderate and severe scenarios now rather than waiting for final measures.

FAQ

Are the new U.S. tariff probes already tariffs?

Not always. Some are investigations and some already include announced response frameworks. Buyers should treat them as live sourcing risks even before a final duty line appears.[1][2][3][4][5][6][7]

Which sectors are most exposed?

The clearest exposure sits in freight-heavy import programs, electronics, pharmaceuticals, copper-intensive manufacturing, and wood-product supply chains.[1][2][3][4][5][6]

Is shifting country of origin enough?

Usually not by itself. The real issue is whether upstream inputs, derivative content, and documentation still leave the product exposed.[2][3][4][5][6]

What is the biggest hidden risk?

Weak visibility. Many companies know their supplier but do not know their true upstream dependency well enough to respond quickly.

Who is least exposed?

Importers with strong BOM discipline, lane visibility, contract protection, and realistic alternate-source options.

Conclusion

The commercial significance of these probes is not that they may produce another round of tariffs. It is that they push trade risk deeper into the operating model. Freight, derivative content, supplier readiness, and documentation discipline are now part of the same conversation.[1][2][3][4][5][6][7]

On paper, these investigations are about national security, strategic industries, and industrial resilience. In practice, they will reward the importers that already know where their weakest supplier file, most fragile lane, and least-defensible origin claim sit.

The upside is real, but only for buyers with enough sourcing control to act before the final rules force the issue.

Sources & References

- USTR, USTR Finds That China’s Targeting the Maritime, Logistics, and Shipbuilding Sectors for Dominance Is Actionable Under Section 301

- Federal Register / BIS, Section 232 National Security Investigation of Imports of Semiconductors and Semiconductor Manufacturing Equipment

- Federal Register, Notice of Request for Public Comments on Section 232 National Security Investigation of Imports of Pharmaceuticals and Pharmaceutical Ingredients

- Federal Register, Notice of Request for Public Comments on Section 232 National Security Investigation of Imports of Copper

- Federal Register, Notice of Request for Public Comments on Section 232 National Security Investigation of Imports of Timber and Lumber

- Federal Register, Addressing the Threat to National Security From Imports of Timber, Lumber, and Their Derivative Products

- USTR, USTR Section 301 Action on China’s Targeting of the Maritime, Logistics, and Shipbuilding Sectors for Dominance

- USTR, Fact Sheet: USTR Takes Action to Bolster U.S. Shipbuilding

- White House, Addressing Certain Tariffs on Imported Articles

- Reuters, Trump Orders New Tariff Probe Into U.S. Copper Imports