For U.S. importers, the most important trade story right now is no longer whether the Trump-era emergency tariffs were aggressive policy. That question has already been overtaken by a more practical one: how, and how fast, companies can recover the cash they already paid. What is the US Tariff Refund Fallout?

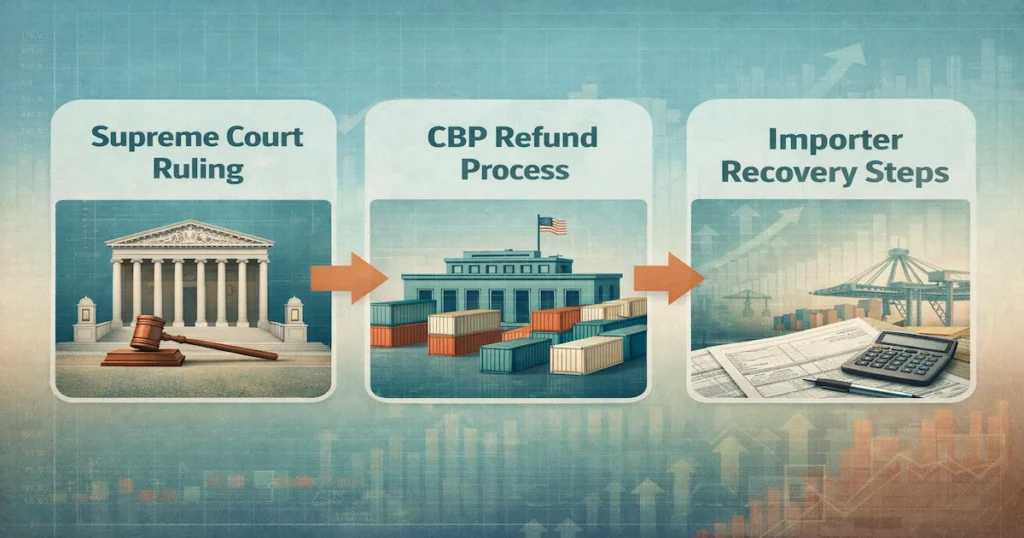

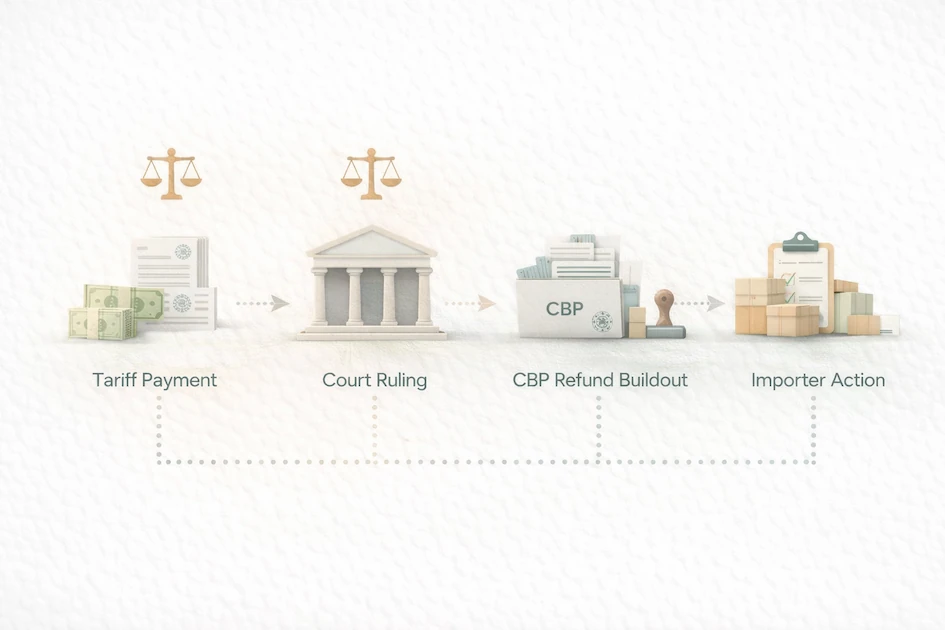

The Supreme Court’s February 2026 ruling striking down the broad IEEPA-based tariffs has shifted the issue from tariff policy to refund execution. CBP is now building a refund mechanism, while thousands of importers are also turning to the U.S. Court of International Trade to preserve or accelerate claims. For finance teams, customs brokers, and sourcing managers, this is not abstract legal news. It is a working-capital event with compliance consequences.

From a sourcing perspective, the story matters because refunds do not arrive neatly just because a tariff was ruled unlawful. In practice, the money only comes back if entry data is usable, importer records are complete, and someone inside the business is actually managing the claim path. What buyers often miss is that the operational burden can quickly outweigh the legal headline. The companies that recover fastest are unlikely to be the loudest. They will be the ones with clean entry files, disciplined broker coordination, and a clear decision on whether to wait for CBP’s system or pursue court-based options.

What Happened

In February 2026, the U.S. Supreme Court ruled that the International Emergency Economic Powers Act did not authorize the broad global tariffs imposed by the Trump administration. That decision put a very large pool of tariff collections into question and immediately created two parallel tracks.

The first track is administrative. CBP has been developing a refund process intended to return unlawfully collected duties without forcing every importer into litigation. The second track is judicial. Importers, including many smaller firms as well as major multinationals, have filed suits in the Court of International Trade seeking refunds and clarity on process.

That split matters. On paper, it suggests optionality. On the ground, it creates uncertainty. Importers now have to decide whether to rely on a future CBP mechanism, preserve claims through litigation, or do both depending on their exposure, records, and risk tolerance.

What This Is — and What It Is Not

This is a cash recovery and compliance management story.

It is not simply a political reversal. It is not automatically a universal refund windfall. And it is not a signal that customs complexity is about to get easier.

The ruling removed the legal basis for those tariffs, but it did not instantly solve the mechanics of repayment. The government still has to determine how claims are identified, validated, processed, and paid. Importers still need to establish which entries were affected, whether duties were passed through contractually, what role customs brokers played in filing, and how internal finance teams will account for potential recoveries.

There is also a practical distinction between eligibility and recoverability. A company may have paid duties that are ultimately refundable, but recovering that cash can still depend on documentation quality, entry traceability, timing, and whether disputes arise over assignments, protests, or intermediary arrangements.

Why This Matters for Buyers and Importers

The commercial impact starts with working capital. Some importers absorbed these duties directly. Others passed part of the cost through to customers. Others still treated them as margin compression they had no real ability to offset. A refund changes that equation, but not evenly.

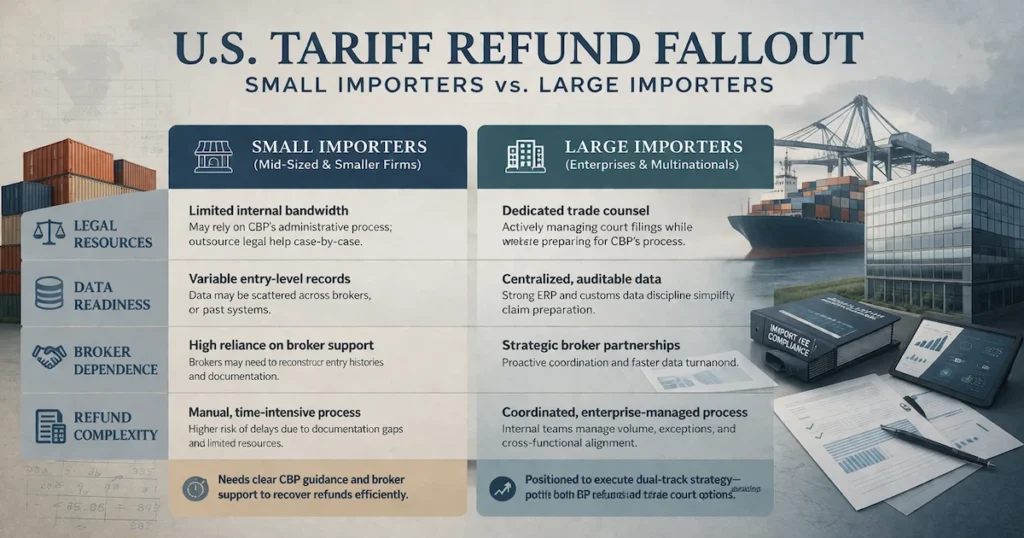

For companies with high import volumes, even partial recovery can affect quarterly cash planning, inventory strategy, and borrowing needs. For smaller importers, the issue is often more basic: whether the refund is large enough to matter, but too small to justify a long legal process. That is where CBP’s refund system becomes important. If it functions cleanly, it could make recovery viable for firms that would otherwise walk away.

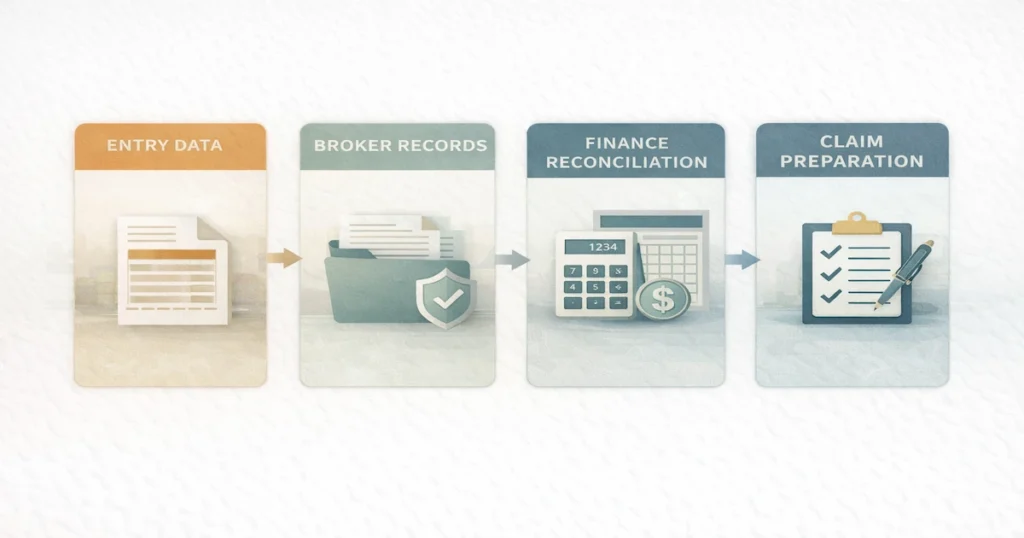

Broker workload is another underappreciated issue. Brokers may need to help reconstruct entry histories, identify affected filings, reconcile importer of record details, and respond to questions about line-level treatment. Where this breaks down is often not in the legal theory but in the file structure. If the importer’s customs data lives across disconnected systems, legacy spreadsheets, email threads, and broker portals, the claim becomes slower and more expensive before anyone even debates entitlement.

There is also a margin-management angle. Some importers will need to decide whether refund proceeds should repair past losses, offset future pricing pressure, or be shared with customers under existing contractual arrangements. That is especially relevant where sales contracts included duty pass-through clauses, price adjustment language, or ambiguous cost-allocation terms.

The Operational Reality Importers Are Walking Into

A clean refund environment would mean CBP matches affected entries, validates payment, and issues reimbursement with limited friction. That is the aspiration. The more realistic scenario is phased processing, exception handling, and a long tail of entries requiring manual attention.

Documentation burden is likely to be the first real constraint. Importers should expect to validate entry numbers, dates, tariff treatment, amounts paid, and importer-of-record identity across potentially large filing populations. Businesses that changed brokers, acquired entities, switched ERP systems, or restructured legal entities during the tariff period may face additional complexity.

Smaller importers are especially exposed here. Large multinationals usually have internal trade teams, outside counsel, and broker management processes. Mid-market firms often do not. They may have the legal right to a refund but lack the internal discipline to assemble the claim efficiently. That asymmetry matters because the policy outcome may be broad, while the actual recovery outcome will be uneven.

In practice, this is where compliance fallout becomes more interesting than the headline tariff story. A refund process forces importers to confront their customs recordkeeping quality. It exposes whether entry data is auditable, whether brokers were managed actively or passively, and whether finance and trade teams can reconcile the same transaction set. On paper this is an administrative clean-up exercise. On the ground it is often a stress test for customs governance.

The Court Option Versus the CBP Option

Some importers are already pursuing relief through the Court of International Trade, and that route may remain important for preserving rights, shaping procedures, or accelerating contested claims. But litigation is not a universal solution for US tariff refund fallout.

For very large exposures, legal action may make commercial sense. For smaller exposures, the economics are more fragile. Filing costs, outside counsel fees, internal management time, and uncertainty around timing all matter. That is why the design of CBP’s refund system is so important. If the administrative path is accessible and reasonably automated, it could reduce the need for many smaller claimants to litigate at all.

Still, importers should not treat this as a simple “wait and see” situation. Waiting can be rational, but only if the company is actively preparing. That means identifying affected entries now, preserving broker communications, reviewing whether protests or related filings already exist, and understanding what deadlines or procedural developments could alter the recovery path.

A Practical Decision Framework

The right next move depends less on ideology than on claim size, data quality, and internal capability.

A company with a large duty exposure, organized customs records, and access to counsel may prefer to preserve optionality through court while also preparing for a CBP-administered solution. A mid-sized importer with moderate exposure and decent records may choose to prepare all documentation and wait for clearer CBP guidance before escalating. A smaller importer with thin internal capacity should focus first on building an accurate entry universe and confirming whether the potential recovery is large enough to justify outside support.

What buyers often miss is that speed and recoverability are now partly operational choices. The government’s process will matter, but internal readiness will matter too. Companies that treat this as a finance-only event may lose time. Companies that treat US tariff refund fallout as a trade-compliance project with finance implications are more likely to recover efficiently.

Buyer Action Checklist

- Identify the full universe of entries that may have been affected by the invalidated tariffs.

- Reconcile duties paid by entry number, date, importer of record, and customs broker.

- Preserve broker statements, payment records, entry summaries, and any post-entry communications.

- Review customer and supplier contracts for duty pass-through or reimbursement language.

- Coordinate finance, legal, customs, and sourcing teams around one recovery plan.

- Monitor CBP guidance and trade court developments at the same time, not sequentially.

- Estimate refund value by business unit or product category to prioritize effort.

- Flag data gaps now, especially where systems, brokers, or entities changed during the tariff period.

FAQ

Will importers automatically receive tariff refunds?

Not necessarily. CBP is building a refund system, but importers should not assume every affected entry will be resolved without supporting data or follow-up.

Do smaller importers need to sue to recover overpaid duties?

Not in every case. The importance of CBP’s administrative refund process is that it may allow many claimants to recover without full litigation. But smaller firms still need organized records to benefit from that path.

What is the biggest operational risk right now?

Poor entry-level documentation. The legal story is clear enough to drive action, but the recovery process may slow down where importer records, broker files, or entity histories are incomplete.

Should importers wait for CBP or file in trade court?

That depends on exposure size, procedural posture, and internal readiness. Larger claims may justify preserving court options. Smaller claims may lean more heavily on an efficient CBP process, assuming documentation is in order.

Why does this matter to sourcing teams, not just customs teams?

Because refunds affect landed cost recovery, margin repair, supplier negotiations, and future pricing decisions. This is not only a legal or customs event. It feeds back into purchasing and commercial planning.

Sources & References

- Reuters: U.S. customs agency expects tariff refund system to be ready within 45 days; report says CBP collected tariff revenue from roughly 330,000 importers and is preparing a refund system that would not require every importer to sue. Reuters

- Reuters: Thousands of lawsuits have been filed in the U.S. Court of International Trade by companies seeking tariff refunds; the court is emerging as a key venue for process-setting test cases. Reuters

- Reuters: The U.S. Supreme Court ruled on February 20, 2026 that IEEPA did not authorize the broad Trump-era tariffs at issue. Reuters

- Reuters: More than $175 billion in tariff collections may be exposed to refund claims following the ruling, according to reporting citing Penn Wharton estimates. Reuters

- Reuters: CBP later reported its refund-system build was materially underway but still incomplete in March 2026. Reuters